The road to investment success is unavoidably long and bumpy. When was any journey worth taking smooth, uneventful and unemotional?

Success is assured, but only if we stay on the road. If we leave the road in the short term by selling investments or otherwise abandoning a long-term investment strategy, we cannot expect to end up where we hoped.

Yet millions of private investors make this simple error. That’s a tragedy.

But don’t take my word for staying on the road; read legendary billionaire investor Howard Marks’ excellent memo “Selling Out”:

“Reducing market exposure through ill-conceived selling—and thus failing to participate fully in the markets’ positive long-term trend—is a cardinal sin in investing.

That’s even more true of selling without reason things that have fallen, turning negative fluctuations into permanent losses and missing out on the miracle of long-term compounding.”

In case we did not understand first time, he continues:

“What about the idea of selling because you think a temporary dip lies ahead that will affect one of your holdings or the whole market?”

And answers:

“There are real problems with this approach:

- Why sell something you think has a positive long-term future to prepare for a dip you expect to be temporary?

- Doing so introduces one more way to be wrong (of which there are so many), since the decline might not occur.

- Charlie Munger, vice chairman of Berkshire Hathaway, points out that selling for market-timing purposes actually gives an investor two ways to be wrong: the decline may or may not occur, and if it does, you’ll have to figure out when the time is right to go back in.

- Or maybe it’s three ways, because once you sell, you have to decide what to do with the proceeds while you wait until the dip occurs and the time comes to get back in.

- People who avoid declines by selling too often may revel in their brilliance and fail to reinstate their positions at the resulting lows. Thus, even sellers who were right can fail to accomplish anything of lasting value.

- Lastly, what if you’re wrong and there is no dip. In that case, you’ll miss out on the ensuing gains and either never get back in or do so at higher prices.

So, it’s generally not a good idea to sell for purposes of market timing. There are very few occasions to do so profitably and very few people who possess the skill needed to take advantage of these opportunities.”

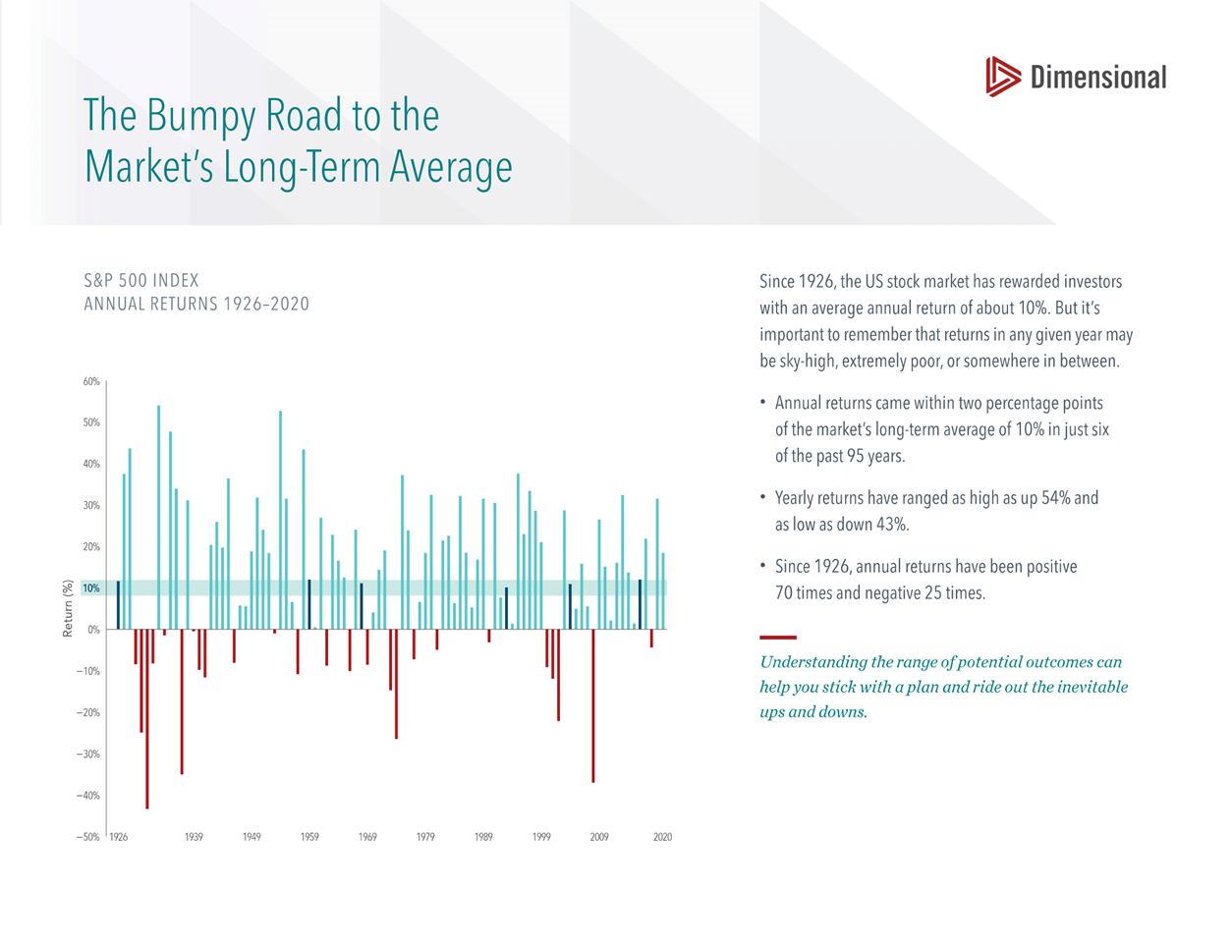

How bumpy might the road be? Look at the S&P 500 (which we use as a proxy for global stock markets) graph below:

Going back 95 years, there have been plenty of ups and downs. About 75% of the time returns were positive. It is the 25% of negative returns that force people, mistakenly, off the road. That is not as many bumps as people might think, is it?

Going back 95 years, there have been plenty of ups and downs. About 75% of the time returns were positive. It is the 25% of negative returns that force people, mistakenly, off the road. That is not as many bumps as people might think, is it?

Were the bumps worth it? I would say so. Let’s take the average return above, add some global diversity and make an allowance for charges.

£100 per month invested since 1992 could now be worth £100,000, tax-free. Your total contributions would have been £36,000.

You could have almost trebled your money, and all you had to do was set up a direct debit and ignore it for 30 years.

That is money just waiting to be given to us, how much easier do we want it?